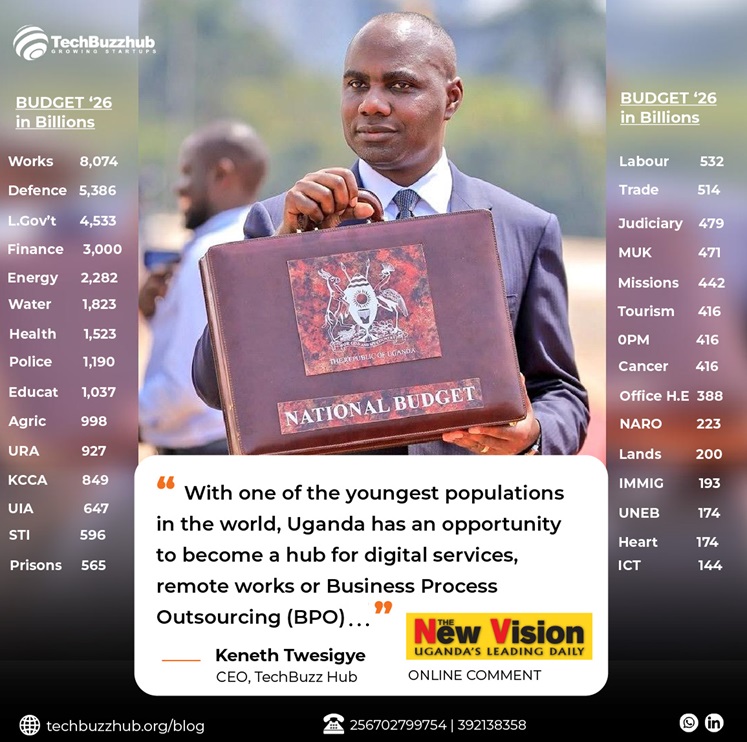

Digital Economy: Uganda’s Hope for Employment if Budgeted

For as long as I can remember, Uganda has sung the song of Agriculture for transformation. This narrative must evolve given the overwhelming population growth by more than double by 2050. It is not with-standing that the digital economy presents a great opportunity to a…

DELIVERING VALUE TO EACH AND EVERY CUSTOMER!

Tough times don’t last but tough people do, two years ago, the headlines along all global news networks was the rocket speed spreading pandemic that saw many industries close down, the fear in the air was evidenced by the empty streets, hallows, corridors market places,…

BOARD OF DIRECTORS VS BUSINESS SUSTAINABILITY – TRAINING

How can we fully benefit from hiring a board of directors/advisors? This training is a continuation from the previous training that was about hiring a board of directors. We want to have you understand what and how you can fully benefit from the board of…

FINDING THE BOARD OF DIRECTORS – TRAINING

How can I get a growth oriented Board of Directors/advisors? This article today is brought to you by TechBuzz Hub in association with its partners the mastercard foundation and the innovation village among others. In a special way today, we bring you Mr. Patrick Obita. …

MANAGING HUMAN RESOURCE – TRAINING

How do I ensure lasting results from my team? Moving forward from the previous training that involved getting your team to work together to produce results, we arrive at managing human resources. In this case Ruth Kamuntu would like to speak to the hearts of…

TEAM BUILDING – TRAINING

How can my employees relate work and achieve? The ARTICLE is brought to you by the team from TechBuzz hub after the very webinar about the same that had Mr. Roland Tayebwa, a proud father, consultant trainer and CEO, DIRECTOR and FOUNDER at Bwongo consult,…

HIRING A STARTUP TEAM – TRAINING

How to build a team that will not sink your startup? Presented by Ms. Ruth Kamuntu a senior human resource manager working with Gotham and the malaria consortium. She is so good that to rephrase her presentation would easily dilute her expertise. So with little…

FINDING A CO-FOUNDER’S

How can I find the right partner for my business? We start a new series of webinars with a new theme “team training” that is actually going to move forward from ideas, now we expect you to have a business and seen it start, however…

FINANCIAL PROJECTIONS IN BUSINESS PART 2 – TRAINING

How do I prepare financial projections for my business? Once again we come to you with financial projections. You may be wondering why, for any business to survive, an entrepreneur must be able to look through the future, to achieve his goals. He must have…

LEGAL REQUIREMENTS OF A BUSINESS – TRAINING-2

How can I handle registration and taxation of my business? Yes, we understand that the topic is very crucial in the well-being of your business and still we want you to have a better understanding of these concepts and ideas. That is why we again…